About this resource

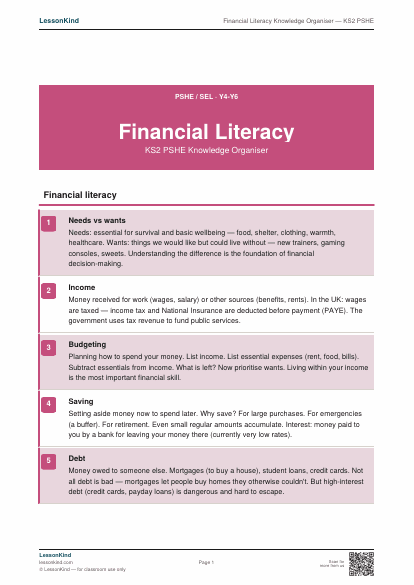

A KS2 PSHE knowledge organiser on financial literacy — needs vs wants, saving, budgeting, income, debt, and making good financial decisions.

What's included

- Print-ready PDF — A4 and US Letter compatible

- No sign-up required — download instantly

- Free to use in your classroom

More like this

More PSHE & SEL resources

Feelings and Emotions — Vocabulary Mat

Twenty emotion words grouped by intensity. Helps children name and talk about feelings.

Friendship Rules

Eight friendship rules that build a kind, inclusive classroom culture.

Growth Mindset — Fixed vs Growth

Compare fixed-mindset and growth-mindset thinking. Rewrite negative self-talk.

Anti-Bullying Class Pledge

A class pledge poster — every child signs and it goes on the wall. Includes definitions of bullying types.

Mindfulness Breathing Techniques

Four kid-friendly breathing techniques to help students calm down or refocus.

Conflict Resolution — Using I-Statements

Turn finger-pointing into clear communication with the I-statement formula.

This page contains affiliate links. We may earn a commission at no extra cost to you.

Stay Safe Online with NordVPN

Protect your connection on school networks and at home. NordVPN is trusted by millions — recommended for teachers and students alike.

Get NordVPN →